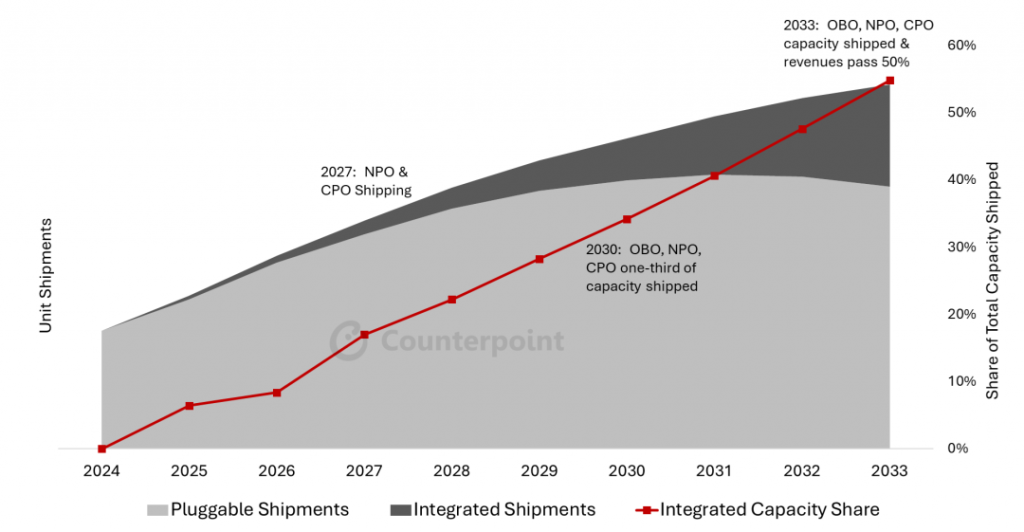

A recent report by Counterpoint Research forecasts a remarkable surge in the market for Near-Packaged Optics (NPO) and Co-Packaged Optics (CPO) solutions, which are expected to be the primary drivers of in-package optical IO technology revenues over the next decade. According to the report, OBO (On-Board Optics), CPO, and NPO solutions are projected to achieve a compound annual growth rate (CAGR) of 50% through to 2033, marking a significant shift in the landscape of AI computing infrastructure.

Source:Counterpoint Research Silicon Photonics(SiPh) and Co-Packaged Optics(CPO) Report

These integrated optical solutions are bringing about massive improvements in transport capacity and processing capabilities, particularly for AI systems. By 2033, more than half of all revenues and shipped capacities in this sector are anticipated to stem from integrated semiconductor optical IO solutions. The momentum behind OBO, NPO, and CPO is undeniable, as they enable extensive bandwidth scaling, lower power consumption, and facilitate the dense, high-bandwidth fabrics necessary for AI clustering at scale.

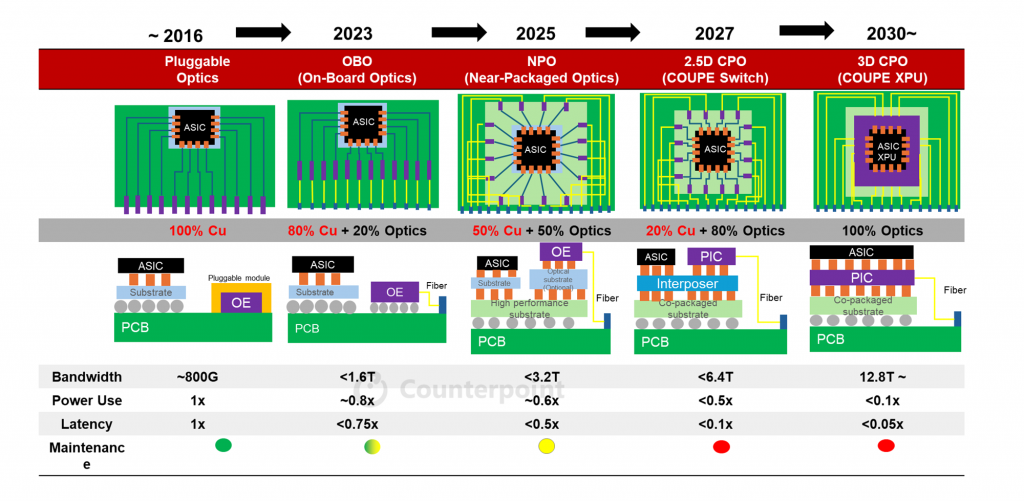

CPO, in particular, is poised to bring about the most significant generational shift in AI computing by enabling extensive bandwidth scaling and AI supercomputing scaling. Leo Liu, associate director at Counterpoint Research, compares this transition to the shift from ADSL to FTTH broadband, but at the chip level. All this additional speed and efficiency is going to usher in the next stage of AI computing, he remarked. While OBO, with products from companies like Applied Optoelectronics, saw wider adoption in 2023, CPO represents the major game-changer, with nearly the entire transport layer being optical.

Despite the enthusiasm, the research firm notes that the evolutionary path towards widespread CPO adoption will be gradual. Key players such as NVIDIA, Intel, Marvell, and Broadcom are at the forefront of CPO developments. However, by 2027, the broad adoption of NPO and CPO is expected to drive integrated revenue growth to triple digits year-over-year, with the share of shipped capacity reaching double digits.

The shift from copper to optical technologies is becoming increasingly evident as AI systems consume more power in data centers. This transition promises increased bandwidth with reduced power consumption. Research Associate David Wu highlights that as we progress from OBO to NPO to CPO, less copper is utilized at each stage, resulting in non-linear performance enhancements. Ultimately, a generational leap in performance of up to 80 times can be expected, with 3D CPO solutions likely outperforming current technologies by a significant margin.

Source:Counterpoint Research Silicon Photonics(SiPh) and Co-Packaged Optics(CPO) Report

In essence, the embedded optical modules market is on the cusp of a transformative era, with OBO, NPO, and CPO solutions leading the charge towards higher bandwidth, lower power consumption, and unprecedented levels of AI computing performance.